Long Iron Condor vs. Short Iron Condor: Options Strategy Guide

Discover the core differences between a long iron condor and a short iron condor. Learn to calculate payoffs, manage risks, and trade volatility.

In the financial markets, most retail investors operate under the assumption that you can only make money when an asset moves aggressively in a specific direction. However, professional options traders understand that markets spend a significant portion of their time consolidating, moving sideways within well-defined ranges. The iron condor option strategy is the premier market-neutral vehicle designed specifically to extract consistent premium income from these range-bound market environments. Instead of betting on a directional breakout, an iron condor trader is effectively placing a bet on a stock doing absolutely nothing of statistical significance.

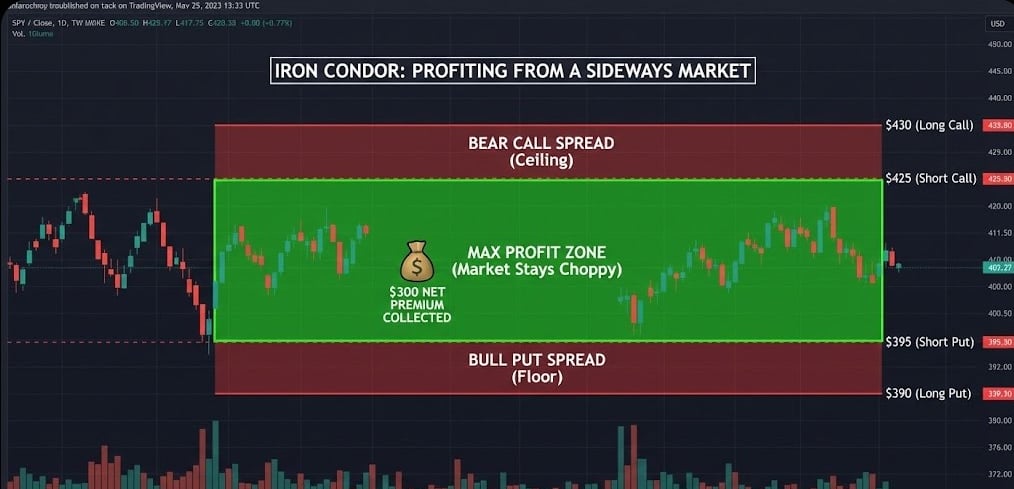

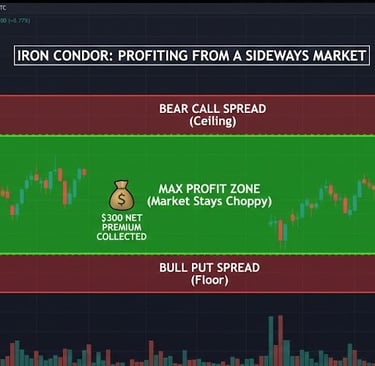

To master the foundational framework of how an iron condor operates, a trader must understand its sophisticated four-legged structure. Unlike simple standalone contracts or two-legged vertical spreads, an iron condor is a combination of two distinct income-generating spreads deployed simultaneously on the exact same underlying asset and sharing the exact same expiration date. It is constructed by combining an out-of-the-money bear call credit spread above the current stock price with an out-of-the-money bull put credit spread below the current stock price.

This four-contract symmetry creates a structural corridor or "profit pocket" for the trade. The underlying architecture involves a highly coordinated execution:

The trader sells an out-of-the-money put option at a specific lower strike price and buys an even further out-of-the-money put option to define and limit the downside risk. This forms the lower wing of the condor.

Simultaneously, the trader sells an out-of-the-money call option at a specific higher strike price and buys an even further out-of-the-money call option to define and limit the upside risk. This forms the upper wing of the condor.

The core philosophy driving this strategy is the exploitation of a dual-sided boundary line. Because both sides of the trade are structured as credit spreads, the trader receives an immediate, upfront net credit premium the moment the complete package order is filled. This net credit represents the absolute maximum profit potential for the position. The trader’s ideal macroeconomic scenario is for the underlying equity to remain completely trapped within the safe neutral zone situated between the two inner short strike prices.

As long as the stock price fails to experience an explosive breakout or a catastrophic breakdown before the expiration clock runs out, all four options contracts will naturally decay toward zero. When expiration day arrives and the stock settles cleanly within the expected range, the contracts expire completely worthless. The brokerage platform immediately releases the maintenance margin requirements back into the available account balance, and the upfront credit collected at entry becomes a hundred percent realized net profit. This makes the iron condor an exceptionally popular strategy for institutional and retail income generators who favor high-probability outcomes over directional speculation.

What is an Iron Condor Option Strategy and How Does It Work?

Constructing a highly profitable short iron condor credit setup requires moving away from speculative guessing and implementing a strict, mathematical blueprint on the options chain. Because this strategy involves managing four separate contracts simultaneously, meticulous execution during the setup phase is the single greatest factor that determines whether your position expires completely worthless or faces a stressful risk management scenario. To build a premium-selling engine that yields consistent results, an active options trader must carefully calibrate their asset selection, strike spacing, and time horizons.

The very first layer of a professional iron condor setup is filtering for the proper underlying asset. Since the objective of this trade is to profit from a stock moving completely sideways, you must target highly stable, range-bound equities. Ideal candidates typically include broad market index funds or heavily traded sector exchange-traded funds. These multi-asset vehicles naturally resist the sudden, erratic individual corporate shocks—such as sudden management shakeups or product failures—that routinely derail individual stocks. Furthermore, absolute liquidity is non-negotiable. You must look for options chains that feature massive open interest and razor-thin bid-ask spreads. High liquidity ensures you can enter and exit all four legs of the trade simultaneously with minimal slippage, keeping your execution costs incredibly low.

Once a premier, liquid asset is isolated, the strategist must determine the position of the two inner short strikes, which serve as the foundation of the credit collection. This phase relies heavily on the use of delta as a direct proxy for probability:

The Downside Short Put: Traders generally look to sell a put option with a delta value ranging between fifteen and twenty-five. This positions the lower boundary far beneath the current stock price, giving the asset a significant statistical cushion against normal market pullbacks.

The Upside Short Call: Conversely, the trader sells an out-of-the-money call option, also targeting a fifteen to twenty-five delta. This establishes an upper boundary well above the current market price, protecting the position from standard bullish runs.

Targeting these specific delta boundaries balances probability and premium. It allows the trader to establish a wider profit corridor, ensuring a high mathematical probability that the stock will stay contained within the boundaries, while still extracting an attractive premium amount from the market.

The next structural step involves placing the outer long wings, which act as the absolute risk ceiling for the trade. To construct a true, balanced iron condor, the distance between the short put and the long put must perfectly match the distance between the short call and the long call. This uniform distance is known as the spread width. If you select a tight spread width, you severely limit the maximum amount of capital you can lose on the trade, but you will also collect less upfront credit and face higher commission drag across your accounts. If you broaden the spread width, you extract a much larger initial credit and experience faster premium erosion, but you also expand your maximum collateral risk if the market suffers an unprecedented directional breakout.

The final piece of this premium-harvesting framework is selecting the optimal expiration date, a process governed entirely by the acceleration of theta, or time decay. While options are constantly losing value, their rate of decay scales up exponentially inside the final month of their life cycle. To fully exploit this mechanical acceleration, professional iron condor writers target expiration windows between thirty and forty-five days out. Entering positions within this timeframe captures the sharpest slope of the time decay curve, allowing the premium to evaporate rapidly while keeping the position short enough to avoid long-term macroeconomic regime changes.

For a comprehensive walkthrough on establishing entry criteria and picking the right technical environments, this Iron Condor Options Strategy Tutorial offers excellent professional insight into choosing strike prices and managing position risks effectively. This video is highly relevant because it provides step-by-step guidance on how to calibrate short option deltas and spread widths to optimize your probability of success.

Structuring the Short Iron Condor Credit Setup for Premium Income

When an options strategist prepares to deploy an iron condor, they must make a definitive decision on how they intend to capitalize on the market's current volatility regime. While the short iron condor is widely celebrated as the ultimate range-bound income engine, it represents only one side of this advanced strategy. An options trader can effectively invert the entire structure by buying the condor instead of selling it. Choosing between a long iron condor and a short iron condor requires a deep understanding of opposing market environments, distinct risk profiles, and completely inverted payoff mechanics.

The core dividing line between these two approaches comes down to whether you are a seller of volatility or a buyer of a breakout. To construct a diversified options portfolio, a trader must know exactly when to act as the premium collector and when to act as the volatility speculator.

The Inverted Mechanics of Capital Flow: A short iron condor is entered for a net credit, meaning cash is deposited into your account immediately because you are selling closer-to-the-money options and buying further out-of-the-money wings for protection. Your maximum profit is capped at this initial credit, while your maximum risk is the width of the spreads minus that credit. A long iron condor operates in reverse. It is established for a net debit, meaning you pay capital upfront. You are buying the inner, closer-to-the-money options and selling the outer wings to subsidize the purchase. This upfront debit represents your absolute maximum risk, while your maximum profit is capped at the spread width minus that initial debit.

Opposing Volatility and Directional Thresholds: The short iron condor is explicitly a market-neutral, short-vega play. It is designed to thrive when the underlying stock price gets completely stuck inside the inner short strikes, allowing all contracts to decay away to zero. If volatility contracts or time passes without a major event, the short condor writer wins. The long iron condor, however, is a market-neutral but long-volatility strategy. A long condor trader does not know which way the stock will break out, but they possess a high conviction that a massive, violent price movement is imminent. The trade achieves its maximum payoff if the stock explodes completely through either the upper or lower outer strike boundaries by expiration day.

The Battle Against the Clock and Vega Exposure: Time decay, or theta, is the short iron condor's greatest ally. Every day that a stock consolidates, the value of the short contracts erodes, allowing the seller to retain their credit. For a long iron condor trader, time decay is a constant, unyielding enemy. If the underlying asset stays completely quiet and consolidates within the inner long strikes, the upfront premium paid will steadily melt away, resulting in a total loss at expiration. However, because the long condor features positive vega exposure, it will benefit heavily from a sudden surge in implied volatility prior to expiration, allowing a trader to exit early for a profit if the market begins to price in extreme panic or euphoria.

Managing risks across these two frameworks requires distinct tactical adjustments. When a short iron condor is tested by an aggressive directional rally, the trader often manages the position by rolling the untested side of the spread closer to the market price to collect additional credit, effectively minimizing the net risk on the losing side. Conversely, a long iron condor requires absolute patience for the breakout to mature. Because the maximum loss on a long condor is strictly limited to the initial debit paid at entry, there is no risk of margin expansion or catastrophic overnight gaps. A trader simply waits for the asset to breach its boundaries, or exits the position early if the expected catalyst fails to generate the raw explosive power required to clear the breakeven thresholds.

Long Iron Condor vs. Short Iron Condor: Risk Management and Payoffs

If you want to master more high-velocity market events, check out our other comprehensive trading guides:

➡️VIX Trading Strategy Guide

➡️How to Trade Economic Data

➡️How to Trade Earnings Reports