The Ultimate Portfolio Diversification Guide: Multi-Asset Strategies

Discover the definitive investment diversification strategy. Learn how to build an adaptive, multi-asset portfolio that counters index concentration and volatility.

In the fast-paced arena of financial markets, the pursuit of wealth is often overshadowed by the failure to manage risk. Many amateur market participants enter the space completely fixated on identifying the single next breakout stock or explosive asset class that will deliver overnight returns. However, veteran market specialists and institutional asset managers recognize that long-term survival and compounding success are entirely dependent on defense. An investment diversification strategy is the foundational risk-management architecture designed to insulate capital from the structural volatility of the markets, ensuring that a single negative event cannot inflict fatal damage on an individual's net worth.

At its core, a diversified portfolio strategy operates on a fundamental truth of economic systems: different financial assets respond differently to the exact same macroeconomic conditions. When inflation surges, certain sectors suffer severe margin compression while others experience massive revenue expansion. When interest rates climb, speculative growth equities routinely face aggressive valuation contractions, whereas specific fixed-income vehicles or cash-flow-rich entities see their risk-adjusted appeal improve. To deploy a true portfolio diversification investment strategy, a trader systematically spreads capital across a broad spectrum of non-correlated or negatively correlated assets, ensuring that when one segment of the portfolio faces a cyclical downturn, another segment stands primed to cushion the blow or capitalize on the environment.

To master how this mechanism functions, one must look closely at the vital distinction between unsystematic risk and systematic risk. Unsystematic risk represents the localized hazards unique to an individual company or a specific niche industry—such as a sudden corporate accounting scandal, an unexpected product recall, or a catastrophic supply chain disruption. If a portfolio is heavily concentrated in just one or two favorite equities, the investor is fully exposed to this localized chaos. By implementing a professional diversification strategy and spreading capital across a wide array of businesses and sectors, unsystematic risk is effectively diluted to near-zero. Systematic risk, on the other hand, represents the broad, unpreventable volatility of the entire macroeconomic system, such as global recessions or geopolitical shocks. While diversification cannot completely eliminate systematic risk, it fundamentally dictates how smoothly a portfolio handles these market-wide drawdowns.

Furthermore, building an institutional-grade diversified portfolio strategy requires avoiding a common psychological trap known as superficial diversification. Many self-directed investors mistakenly believe they are safe because they own ten different stocks. However, if all ten of those companies are high-beta technology firms or heavily tied to the semiconductor space, the portfolio is completely synchronized. When a sector-wide correction hits, all ten equities will collapse in unison, completely exposing the illusion of safety. True, structural diversification requires deliberate cross-asset placement, blending defensive value equities, growth instruments, option-hedged positions, and alternative asset classes to build a resilient, multi-layered financial fortress capable of generating consistent yield across any market regime.

What is an Investment Diversification Strategy and How Does It Work?

Translating a broad philosophical appreciation for risk management into a functioning wealth engine requires a deep dive into the equity portion of your portfolio. A masterfully crafted stock diversification strategy goes far beyond randomly purchasing a dozen household corporate names. It requires building a multi-layered, three-dimensional asset framework on your trading hub that spans across distinct market capitalizations, varying investment styles, diverse economic sectors, and global geographic regions. Failing to organize these layers deliberately creates a fragile, highly correlated equity portfolio that leaves you completely exposed to systemic sector corrections.

The first fundamental layer of a robust stock strategy involves distributing capital across the three core market capitalization spectrums: large-cap, mid-cap, and small-cap companies. Large-cap equities represent institutional cornerstones—mature corporations with massive balance sheets, stable global revenue streams, and a documented history of navigating macroeconomic downturns. While these mega-cap names provide vital structural ballast, their top-line expansion naturally faces structural scale limits. To counter this, a growth-oriented portfolio injects a calculated allocation into mid-cap and small-cap companies. Mid-cap firms often occupy the sweet spot of corporate growth, possessing established products but retaining significant room to scale operations. Small-cap companies introduce higher near-term volatility and face tighter credit conditions, but they offer explosive long-term appreciation potential during early economic expansions, ensuring your portfolio captures early-stage market innovators before they achieve mainstream institutional adoption.

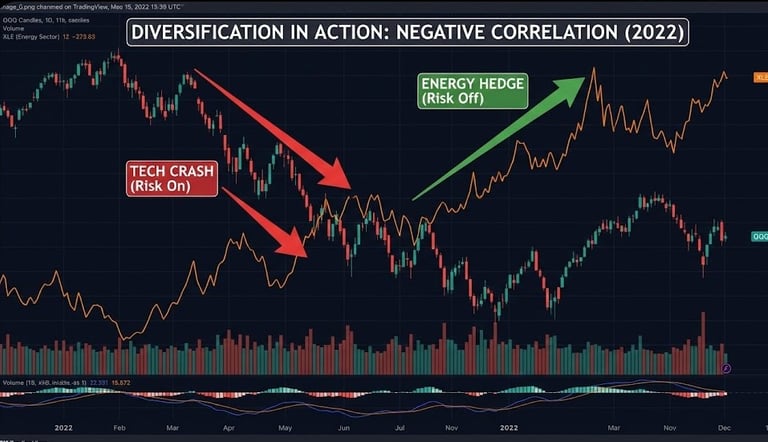

The second critical layer demands absolute style and sector neutrality, which requires a conscious effort to balance growth factors and value factors. In modern markets, equity indices frequently face severe concentration risk, where a handful of hyper-scaling technology and artificial intelligence firms dictate the movement of the entire broader market. While riding a momentum-driven growth wave is highly lucrative, a professional strategist actively hedges this concentration by holding value-oriented sectors, such as energy, industrials, healthcare, and financial services. Growth stocks trade on future earnings expectations and flourish when interest rates decline, while value stocks feature lower earnings volatility, trade at reasonable historical multiples, and frequently provide reliable cash flow through consistent dividend payouts. By maintaining an active factor rotation framework, you ensure that your portfolio automatically extracts gains when capital flows out of expensive growth names and cycles into defensive, tangible asset sectors.

The third dimension of equity optimization requires expanding your horizons beyond domestic borders through geographic diversification. Operating exclusively within your home market exposes your net worth to localized regulatory changes, currency fluctuations, and domestic central bank policy errors. A truly diversified portfolio strategy allocates a meaningful portion of its equity capital to international developed markets and high-beta emerging economies. Developed international markets feature lower historical earnings volatility and a strong structural tilt toward classic value sectors. Conversely, emerging markets in regions like Asia and Latin America act as the central nervous system for global manufacturing, energy infrastructure, and technology supply chains. Gaining exposure to these international corridors ensures you capture explosive economic expansions occurring completely independent of domestic market dynamics.

The final, matching operational piece of this entire stock framework is the implementation of a rigid, systematic rebalancing discipline. Over time, different asset segments perform at different speeds. An exceptional year in technology or growth equities will naturally cause that specific sleeve to expand, distorting your intended risk parameters and leaving your portfolio dangerously top-heavy. To correct this behavioral drift, professional portfolio managers review their allocations periodically, utilizing a strict 5% to 10% drift boundary as an actionable trigger. If a winning sector or asset class expands beyond its target threshold, the rules mandate selling a portion of those overperforming assets and reallocating the cash to purchase underperforming, out-of-favor asset classes. This cold, rules-based rebalancing mechanism systematically strips away emotion, forcing you to execute the ultimate golden rule of the financial markets: selling high to lock in profits, and buying low to acquire discounted assets right before the next cyclical rotation begins.

Designing the Best Stock Diversification Strategy for Long-Term Growth

Achieving true resilience within a modern trading hub requires an investor to evolve past the outdated concept of static, passive allocation. For decades, traditional financial planning relied on the classic assumption that simply buying a broad equity index fund provided automatic, flawless diversification. However, structural shifts in market dynamics have completely upended this paradigm. Modern capitalization-weighted indices have reached unprecedented levels of concentration, where a mere handful of mega-cap technology and artificial intelligence leaders command a massive share of the total index weight. Buying a standard index fund today does not distribute your risk across the economy; instead, it funnels a significant portion of your capital into a highly correlated, single-thematic trade. To protect an equity curve from systemic shocks, an active strategist must deploy an adaptive multi-asset allocation framework that thrives across changing macroeconomic regimes.

To navigate this landscape of hyper-concentration, a professional portfolio architecture must expand beyond traditional public equities. This requires building a robust, multi-layered defensive perimeter across three core alternative asset pillars:

High-Quality Fixed Income and Short-Duration Credit: When equity valuations are rich and macroeconomic policy transitions through an easing cycle, core taxable bonds and short-duration corporate credit serve as an indispensable portfolio anchor. Instead of letting duration—or interest rate sensitivity—dominate your defensive sleeve, focusing on shorter-duration instruments allows you to extract highly attractive yields while insulating your principal from volatile interest rate fluctuations. This fixed-income anchor supplies liquid ballast that reliably mitigates risk when equities experience localized corrections.

Real Assets and Liquid Alternatives: Inflationary pressures can remain structural and sticky due to supply chain re-globalization, energy infrastructure transitions, and shifting global trade policies. Traditional diversifiers can periodically move in lockstep with equities during sudden inflation scares, meaning asset protection is not a one-size-fits-all model. To insulate your purchasing power, an adaptive portfolio maintains dedicated sleeves in real assets, commodities, and systematic liquid alternatives. These tactical instruments possess a low historical correlation to public stock markets, providing an active hedge when both stocks and standard bonds face simultaneous downward pressure.

Option-Hedged Income Overlays: A sophisticated trading platform enhances standard asset holding returns by layering systematic options strategies directly over core positions. When broad market indices exhaust their upward momentum and enter extended consolidation ranges, an adaptive investor uses covered calls, cash-secured puts, and market-neutral spreads to extract consistent cash-flow premiums from the market's idling behavior. This option overlay effectively lowers the portfolio's aggregate cost basis, turns market volatility into a direct source of income, and establishes defined breakeven boundaries that cushion the broader account against sudden, adverse price swings.

The ultimate key to executing an adaptive portfolio diversification guide is aligning your asset deployment with current macroeconomic market cycles. During late-stage economic expansions characterized by high valuations and broadening corporate leverage, the strategist acts with cautious optimism—rightsizing equity risk by tilting toward high-quality large-cap value and defensive international developed equities, where stable fundamentals and lower multiples protect capital. Conversely, as the macro backdrop normalizes or enters an early-cycle recovery phase, the framework dynamically expands into high-quality small-cap names and emerging market corridors to capture early-stage economic growth. By treating asset allocation as a fluid, responsive discipline governed by rigid rules rather than passive inertia, you transform your trading hub into an all-weather financial fortress capable of sustaining steady compounding across any economic environment.

The Adaptive Portfolio Diversification Guide Across Assets and Market Cycles

If you want to master more high-velocity market events, check out our other comprehensive trading guides:

➡️VIX Trading Strategy Guide

➡️How to Trade Economic Data

➡️How to Trade Earnings Reports