$WMT Stock Flight to Safety Squeeze: Critical Trading Levels

Master the $WMT short squeeze setup. Get the critical must-hold support level, tactical entry rules, and the multi-tiered profit targets.

TRENDING STOCKS

The Fundamental Bull Case: Analyzing Walmart's Defensive Moat and Value Leadership

A profound and persistent question shared by retail speculators and institutional asset managers alike is whether is walmart stock a buy today, or if it is time to look elsewhere for long-term portfolio compounding. As broad macroeconomic shifts continue to reshape consumer discretionary spending, analyzing a blue-chip retail giant like Walmart Inc. ($WMT) requires looking past basic storefront foot traffic. True analytical success relies on understanding how the underlying corporation continually modernizes its defensive moat to weaponize absolute value leadership during highly complex economic cycles.

Historically, the firm built an unassailable commercial advantage by mastering supply chain logistics, allowing it to maintain absolute price leadership over regional grocery chains and specialized retailers. During inflationary macroeconomic cycles, this competitive moat becomes a powerful market-share compounding machine. As consumer purchasing power experiences persistent pressure from elevated living costs, a well-documented behavioral shift known as "trade-down traffic" takes hold across the consumer landscape.

The most compelling aspect of this fundamental thesis is that the brand is no longer just attracting its traditional, value-conscious customer base. Instead, industry data demonstrates that a significant percentage of the company's rolling market-share gains are being captured directly from households with an annual income exceeding one hundred thousand dollars. High-income families are increasingly migrating their recurring grocery, household essentials, and pharmacy spending to the platform to protect their real disposable income. This structural demographic expansion changes the long-term cash flow profile of the firm, giving it an unprecedented opportunity to cross-sell higher-margin services to a more affluent customer cohort.

To evaluate whether this operational strength translates into a high-conviction portfolio allocation, an investor must analyze the core pillars that preserve the firm's fundamental business model:

Massive Purchasing Power and Economies of Scale: Operating over ten thousand global physical footprints gives the organization a level of supplier leverage that is completely unmatched in the retail ecosystem. The firm routinely requires vendors to lower wholesale pricing boundaries, allowing it to absorb localized supply chain inflation without compressing its own gross margins or losing price competitiveness at the shelf.

Essential Grocery and Consumables Dominance: Because a massive portion of the company's net sales mix is derived from non-discretionary grocery items, household goods, and pharmacy essentials, its top-line revenue exhibits an incredibly flat, recession-resistant curve. Regardless of broader economic contractions or labor market drawdowns, consumers must continuously replenish basic biological necessities, shielding the firm's balance sheet from structural revenue shocks.

Private Label Optimization Layouts: The corporate parent has aggressively prioritized the scale and premium branding of its internal private labels. Private label products carry structurally higher operating profit margins compared to national brand names. By positioning these value-engineered offerings prominently across digital and physical aisles, the chain enhances its consolidated return on invested capital while offering pinched consumers an attractive alternative at a lower price point.

At this massive operational scale, even minor incremental improvements in operating efficiency result in billions of dollars of free cash flow expansion. While the core retail engine keeps the business fundamentally safe and predictable, it acts as a massive financial launchpad to subsidize high-tech automation and capital expenditure programs. For long-term portfolio managers searching for steady dividend growth and a reliable anchor to absorb broader equity market volatility, the company's capacity to weaponize its scale across varying consumer income brackets solidifies its institutional reputation as an enduring, high-conviction compounder.

📊 Operational Takeaway

A professional analyst evaluates a megacap stock like $WMT not by searching for rapid, triple-digit sales growth, but by monitoring the stability of its operating margins and return on invested capital. If the firm effectively captures and retains the higher-income demographic while using automated logistics to manage its internal inventory overhead, the underlying business maintains a clean structural edge capable of driving steady equity gains over long-term market cycles.

E-Commerce Evolution and High-Margin Diversification Engines

For a multi-decade retail powerhouse, sustaining long-term capital appreciation requires far more than merely expanding physical square footage or optimizing brick-and-mortar grocery margins. In the modern retail environment, digital scale has transitioned from a secondary convenience overlay into an absolute core operational requirement. To transform its equity profile from a low-growth mature dividend payer into an aggressive, multi-channel growth engine, Walmart has executed a massive, multi-billion-dollar digital evolution. By effectively leveraging its unrivaled network of physical stores as localized fulfillment hubs, the company has closed the structural gap with pure-play e-commerce operators, while simultaneously building an array of high-margin, software-driven diversification engines that completely reshape its consolidated profitability profile.

The operational genius of the company's digital transformation relies on its omnichannel fulfillment framework. Instead of building an entirely separate, hyper-expensive network of standalone distribution centers from scratch, the corporation weaponized its existing real estate asset base. Over ninety percent of the domestic population resides within ten miles of a physical brick-and-mortar location. By integrating advanced machine learning algorithms into its inventory management software, the firm converted thousands of its retail supercenters into micro-fulfillment engines capable of executing same-day delivery and rapid curbside pickup. This hybrid infrastructure slashes the historically prohibitive "last-mile" delivery costs that plague traditional online retail, allowing the business to scale its digital marketplace volume while maintaining structural capital efficiency.

Beyond the digital checkout lane, the true driver of long-term margin expansion rests on the rapid scale of its auxiliary corporate ecosystems. In traditional retail, thin margins are an unavoidable operational reality. To break free from this restriction, the firm has systematically duplicated the technology playbooks of modern cloud platforms, introducing a suite of high-margin digital business segments:

The Walmart Connect Retail Media Network: Operating a commerce platform with billions of annual user transactions generates an incredibly valuable ocean of first-party consumer data. The firm has successfully monetized this asset through its proprietary advertising division, Walmart Connect. Brands and third-party sellers pay a premium to route highly targeted advertisements directly to consumers across the company's digital applications and physical in-store displays. Because media networks operate with software-like gross margins, this high-velocity advertising stream filters directly down to improve consolidated operating income.

The Third-Party Marketplace and Fulfillment Services: To compete directly for digital shelf space, the corporation has rapidly expanded its third-party merchant ecosystem. By welcoming independent brands onto its digital store, the firm extracts steady transaction fee revenues without taking on the balance sheet risk of owning the underlying inventory. Furthermore, by cross-selling Walmart Fulfillment Services (WFS), the organization handles the storage, picking, packing, and shipping for these independent merchants, capturing recurring logistics fees while filling its existing distribution network to maximum capacity.

The Walmart+ Subscription Moat: The deployment of a premium membership program serves as a critical behavioral lever for driving consumer lifetime value. Subscribers pay a recurring annual or monthly fee to unlock unlimited free delivery, fuel discounts, and digital streaming bundles. This subscription architecture creates a highly predictable stream of recurring service revenue while driving intense customer lock-in. Data indicates that a subscription member transacts significantly more frequently and maintains a substantially higher average basket size than a non-member, compounding top-line velocity.

This strategic pivot into advertising, fulfillment logistics, and premium subscriptions completely alters how Wall Street values the enterprise. The organization is no longer a simple, capital-heavy brick-and-mortar retail engine vulnerable to localized economic downturns. Instead, it has successfully built a software-and-data ecosystem that extracts continuous monetization out of its massive consumer traffic. By subsidizing its core value pricing with high-margin digital revenue streams, the corporation constructs an incredibly resilient capital flywheel that preserves its long-term market dominance, making the equity an exceptionally compelling vehicle for sustained portfolio growth across any economic landscape.

Valuation Assessment and Technical Entry Roadmaps Post-Correction

Navigating a megacap core holding like Walmart Inc. ($WMT) through a mature market cycle requires a strict separation between short-term noise and long-term structural value. Following a massive, multi-year bull run that pushed the equity to a historical 52-week high of $135.16, the stock recently experienced a sharp, healthy correction. This sudden technical pullback was triggered by a combination of localized inventory-clearing concerns and a bearish research note flagging a temporary moderation in domestic comparable store sales. For emotional short-term traders, this volatility caused immediate anxiety; however, for institutional asset managers and systematic portfolio strategists, this correction has successfully wrung the froth out of the equity, opening up a high-probability technical window to accumulate shares of a dominant value leader at a significant structural discount.

To determine whether the stock represents a high-conviction buy at current levels, an investor must critically evaluate the company’s historically premium valuation multiple. Trading at roughly 38x to 40x forward earnings, the equity undeniably commands a steep valuation premium compared to legacy brick-and-mortar competitors like Target or regional grocery operators. In a traditional retail context, a multiple this high would signal an overextended, high-risk setup with an incredibly thin margin of safety. However, the modern marketplace is no longer a traditional retailer. Wall Street is increasingly willing to support an elevated premium multiple because the quality of the company's underlying cash flow has structurally changed.

The primary driver of this institutional re-rating is the rapid expansion of its alternative, asset-light revenue segments, which now account for approximately one-third of the firm's total operating income (EBIT). High-margin cash flows from Walmart Connect media advertisements, third-party seller logistics fees, and recurring digital membership dues are growing at a rate two to two-and-a-half times faster than physical storefront sales. This structural shift effectively insulates the consolidated corporation from physical retail margin erosion. When an organization can subsidize its low-margin grocery business with software-like digital advertising revenues, it creates a robust fundamental floor that justifies a permanently higher baseline valuation. This explains why the overarching Wall Street consensus remains deeply constructive, with premium investment bank coverage lists maintaining an average long-term price target range between $138 and $144 per share, implying significant asymmetric upside from the post-correction lows.

This structural fundamental safety is further enhanced by a series of powerful macroeconomic tailwinds and capital flexibility buffers. Recent cooling labor market data and softening macroeconomic reports have significantly shifted broader interest rate expectations, easing institutional fears of further aggressive monetary tightening. This cooling economic backdrop has sparked a major sector rotation across the financial markets, driving institutional capital out of hyper-extended, highly speculative technology equities and directly into resilient, blue-chip defensive anchors that possess the raw pricing power to comfortably navigate a slowing economic environment. Furthermore, the organization possesses a massive, hidden financial cushion in the form of approximately $3 billion in potential tariff refunds. Rather than recognizing this massive windfall all at once to artificially inflate a single quarter's earnings report, corporate management has strategically opted to deploy these capital reserves over time into targeted price investments across high-velocity consumables. This deliberate operational deployment ensures that the company can continuously widen its pricing gap against struggling competitors, securing long-term market share dominance even if aggregate consumer demand continues to soften.

From a structural charting perspective, the recent multi-day slide has cleanly reset the stock’s technical indicators, presenting a highly attractive risk-to-reward architecture for active market participants. By mapping out the major horizontal demand nodes and behavioral support levels left behind by institutional block-buying orders, we can construct a definitive technical execution roadmap for accumulating exposure:

The Oversold Institutional Demand Zone ($108 to $112 Area): This localized price pocket represents the primary technical launchpad where the recent correction officially stalled out. As the stock plummeted toward the $108 level, its daily Relative Strength Index (RSI) collapsed into deep oversold territory, printing an extreme reading below 26, while the Williams Percent Range reached maximum oversold exhaustion. This extreme mathematical dislocation triggered massive institutional dip-buying and short-covering, resulting in a powerful single-session rebound on expanding relative volume. This area establishes a high-volume support shelf where large-scale asset managers are actively defending their long-term cost bases.

The Macro Trend Validation Floor ($102 to $105 Area): Serving as the absolute line in the sand for long-term trend followers, this deeper demand corridor represents the ultimate margin of safety level. This zone aligns perfectly with historical structural breakouts and long-term macro moving averages. While a temporary breakdown beneath the immediate $108 shelf is possible during periods of broad market deleveraging, institutional liquidity pools sitting between $102 and $105 are exceptionally dense. As long as the stock remains structurally positioned above this macro floor on a monthly closing basis, the primary secular uptrend remains entirely intact.

The Immediate Overhead Resistance Hurdle ($122.33 Level): On any sustained counter-trend rally, the stock will encounter initial selling pressure at the $122.33 congestion node. This level represents the historical inflection point where early long positions trapped during the initial correction will look to exit at breakeven, creating a temporary ceiling of supply. A decisive, high-volume daily close above $122.33 is required to officially shift the immediate-term technical momentum back into the hands of the bulls.

The Squeeze Trigger and Trend Continuation Line ($134.78 Level): Representing the previous historical peak, this level serves as the ultimate gateway to a prolonged trend expansion. If the price can successfully consolidate its gains above the $122 hurdle and orchestrate a clean breakout past $134.78, it will trigger a massive wave of momentum buying and forced short capitulation. Clearing this final overhead resistance level effectively removes all structural supply nodes, clearing a completely unblocked chart runway for an extension toward the macro targets of $150 to $160 per share.

Ultimately, executing a sophisticated positioning plan on a defensive titan like this requires moving past emotional day-to-day market commentary and relying exclusively on mechanical execution rules. Trying to perfectly time the absolute bottom of a correction is a statistical fool's errand. Instead, an advanced portfolio strategist utilizes localized market pullbacks to scale into a core position via passive limit orders scattered throughout the institutional demand zone. By capturing shares while the retail crowd is panicking over short-term inventory adjustments, you position your portfolio alongside smart money flow. Grounding your investment hub in the undeniable reality of the company's digital margin flywheel allows you to confidently block out short-term noise, transform technical volatility into an asset, and secure an optimized entry price primed for multi-year equity compounding.

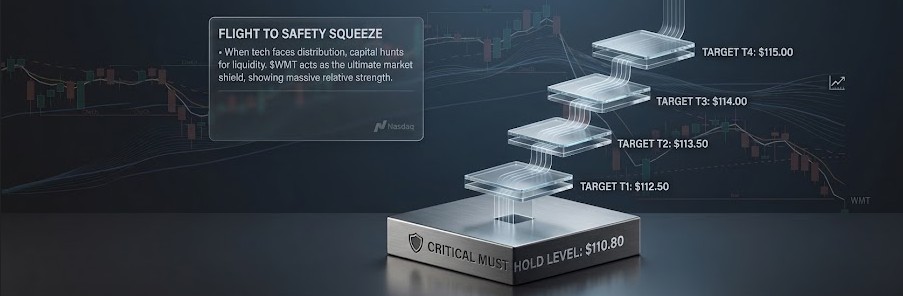

Tactical Playbook: Trading the WMT Flight to Safety Squeeze

When large-cap technology and growth sectors face heavy institutional distribution, market liquidity does not simply evaporate into cash. Instead, institutional portfolio managers systematically rotate their capital into bulletproof, high-relative-strength defensive anchors to shield their gains from macro market drawdowns. This massive sector rotation creates what professional tape readers call a "flight to safety squeeze." As short sellers attempt to fight the broader market's decline by shorting retail names, an aggressive influx of institutional buying completely traps them, winding up the price action like a spring. To successfully navigate this high-probability velocity setup, an active market participant must move past emotional prediction and rely on a strict, rules-based execution playbook built around a definitive must-hold floor and sequential overhead liquidity targets.

The absolute foundation of this entire tactical setup rests on the preservation of a singular, non-negotiable line in the sand: the $110.80 critical must-hold level. In macro market microstructure, this specific price point represents the exact zone where institutional algorithms have heavily stepped in to absorb supply, validating it as a high-volume support shelf. If the underlying asset undergoes a localized intraday pullback, executing long entries immediately adjacent to the $110.80 floor provides an incredibly asymmetric risk-to-reward configuration. Your mandatory stop-loss can be nestled tightly just on the other side of this structural boundary. If the $110.80 area holds firmly on a retest, it confirms that the defensive shield is fully active, locking in the structural launchpad and clearing the runway for an explosive, multi-tiered short-covering squeeze.

Once the support floor is successfully defended, the upward momentum will progress through a series of clear technical milestones. To optimize value extraction from this position, you should monitor your platform’s order book as the asset approaches these specific profit targets:

Target T1 ($112.50): This represents the initial overhead liquidity pool and immediate high-volume congestion node. Clearing this level proves that buyers have successfully absorbed the morning supply, shifting the short-term tape momentum entirely back into the hands of the bulls.

Target T2 ($113.50): An intermediary resistance tier where early momentum buyers will look to scale out of partial positions. Expect localized profit-taking here, making it an excellent zone to lock in a portion of your gains and trail your remaining stop-loss to a risk-free breakeven line.

Target T3 ($114.00): A prominent psychological milestone and historical distribution layer. As the price clears the $114.00 threshold, it aggressively shifts macro sentiment, forcing trailing stop-losses to trigger across surviving short positions and accelerating the velocity of the move.

Target T4 ($115.00): The ultimate extension target for this specific rotation cycle. This area aligns perfectly with a major structural distribution peak on the higher-timeframe chart, representing the optimal zone to completely flat your position and fully realize your accumulated compounding returns.

🛑 Tactical Execution Alert

The Takeoff Rule: Never chase fast-moving green candles into overhead supply. If the asset begins spiking, wait patiently for a clean, low-volume retest of the $110.80 defense zone. If buyers step back up on high relative volume, route your entry mechanically, size your position according to your fractional capital rules, and allow the mathematical probability of the upside targets to efficiently build your equity curve.

DISCLAIMER: Not financial advice. This is a market commentary piece based on current price action and options flow, and conditions can change quickly.